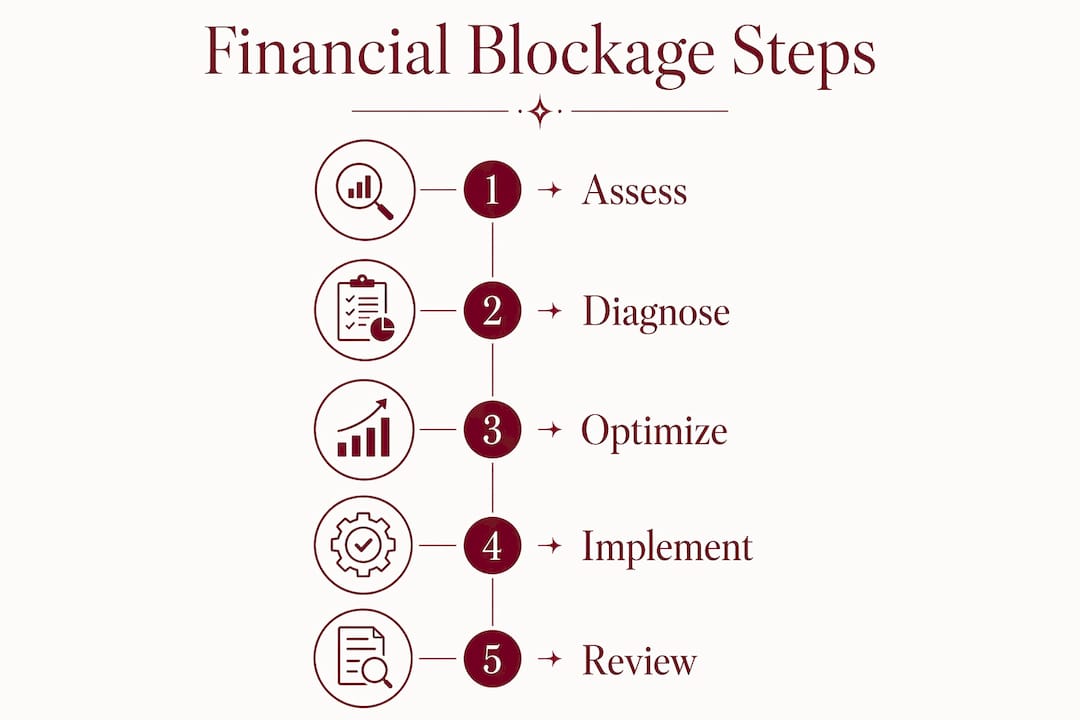

Removing financial blockages in business is the process of identifying and eliminating both mental and operational obstacles that prevent consistent cash flow and growth. Most small business owners focus only on the numbers, but the real problem is often split between subconscious money beliefs and broken financial systems running at the same time. The good news: measurable financial improvements are achievable within 30 days, with sustainable systems built in 90 days. This guide covers both sides, giving you a clear path to eliminate business financial obstacles and restore momentum.

How do mindset and subconscious beliefs create financial blockages in business?

Money blocks are rooted in subconscious beliefs and nervous system responses that quietly sabotage your financial actions. You may avoid sending invoices, hesitate to raise prices, or feel physical anxiety before checking your bank balance. These are not personality flaws. They are patterned responses your nervous system learned, often long before you started your business.

Common money stories entrepreneurs carry include:

- Fear of abundance: Believing that earning more will attract resentment, conflict, or loss.

- Scarcity mindset: Assuming there is never enough, which leads to underpricing and over-delivering.

- Unworthiness: Feeling that charging full price is somehow dishonest or greedy.

- Inherited financial shame: Absorbing family beliefs about money being dangerous or corrupting.

These stories do not stay in your head. They show up as patterns in your business energy that affect pricing decisions, client relationships, and revenue cycles. Recognizing the story is the first step. Changing the behavior that follows is the second.

Nervous system regulation before financial tasks makes a concrete difference. Spending two minutes on slow breathing or journaling before reviewing your accounts reduces the stress response that triggers avoidance. That small act shifts your brain from threat mode into problem-solving mode.

Pro Tip: Before your next financial review, write one sentence completing this prompt: “Money in my business is ___.” Your answer reveals the belief driving your behavior. Rewrite it as a fact you want to be true, and read it aloud before every money task for 30 days.

Aligned action reinforces the new belief. If your new story is “I am paid well for my work,” the aligned action is sending that overdue invoice today, not next week. Mindset work without behavior change produces no financial result.

What are the essential financial management tools and practices to diagnose and clear blockages?

Diagnosing a financial blockage requires visibility. You cannot fix what you cannot see. Subdividing your business bank accounts into 6–10 accounts for specific purposes, such as operating expenses, taxes, payroll, and profit, gives you an accurate picture of true cash availability at any moment.

The first diagnostic action is a full cash position assessment completed within 48 hours. List every dollar coming in and going out over the next 30 days. This single exercise reveals whether you have a revenue problem, a collections problem, or a spending problem. Most owners discover it is a collections problem.

Electronic invoicing reduces payment collection times by up to 80% compared to manual invoicing. That is not a minor improvement. For a business waiting 45 days to collect on a $10,000 invoice, switching to electronic invoicing could mean collecting in under 10 days.

Weekly financial reviews covering cash position, revenues, costs, and key performance metrics are the single most effective habit for early problem detection. Most business owners review finances monthly or quarterly. By then, a small cash gap has become a crisis.

| Tool or Practice | What It Does | Why It Matters |

|---|---|---|

| Multiple bank accounts | Separates cash by purpose | Prevents accidental overspending |

| Electronic invoicing | Sends and tracks invoices digitally | Cuts collection time by up to 80% |

| Accounts receivable aging report | Tracks unpaid invoices by age | Identifies overdue accounts before they become losses |

| 13-week cash forecast | Projects weekly cash in and out | Gives early warning of shortfalls |

| Weekly financial review | Reviews cash, revenue, and costs | Catches problems before they compound |

Pro Tip: Set a recurring 30-minute calendar block every Monday morning labeled “Money Date.” Review your cash position, check your aging report, and confirm your top three revenue actions for the week. Consistency here is worth more than any single financial fix.

What step-by-step financial turnaround strategies rapidly remove business financial blockages?

A structured triage approach outperforms impulsive cost-cutting every time. The goal in the first 30 days is cash preservation and stabilization, not a complete business overhaul.

The 30-day triage plan

- Day 1–3: Freeze non-essential spending. Pause all subscriptions, discretionary purchases, and non-critical vendor payments. This is not permanent. It buys you time to assess.

- Day 1–3: Complete a full cash position assessment. List all cash on hand, receivables due within 30 days, and payables due within 30 days. This is your baseline.

- Day 4–7: Accelerate collections. Assign one person, even if that person is you, to own accounts receivable. Call every invoice over 15 days old. Offer a small early payment discount if needed.

- Day 7–14: Renegotiate supplier terms. Extending payment terms from net 30 to net 45 or net 60 with key suppliers eases immediate cash pressure without cutting services.

- Day 14–21: Cut operating expenses by 15–25%. Companies in acute financial distress typically need to reduce operating expenses by 15–25% to reach break-even. Cut costs that do not directly support revenue generation first.

- Day 21–30: Build a 13-week cash forecast. Map every expected cash inflow and outflow for the next 13 weeks. Update it every Monday. This forecast becomes your decision-making tool for the next 90 days.

- Day 30–90: Build sustainable systems. Formalize your invoicing process, set up account subdivisions, and schedule weekly reviews. These systems prevent the next blockage from forming.

Pro Tip: When cutting expenses, protect three categories: your top revenue-generating marketing channel, your best-performing team member, and your client delivery quality. Cutting these to save cash almost always costs more in lost revenue than the savings are worth.

| Phase | Timeframe | Primary Goal |

|---|---|---|

| Triage | Days 1–7 | Stabilize cash, freeze spending |

| Collections push | Days 4–14 | Accelerate receivables, reduce aging |

| Cost restructuring | Days 14–21 | Cut 15–25% of operating expenses |

| Forecasting | Days 21–30 | Build 13-week cash visibility |

| Systems building | Days 30–90 | Create durable financial processes |

How can entrepreneurs integrate mindset shifts with financial actions for lasting results?

Rewriting your money identity combined with nervous system regulation before financial tasks produces lasting removal of financial blocks. The key word is “combined.” Belief work alone produces inspiration. Financial action alone produces burnout. Together, they produce durable change.

Financial stress impairs executive function, which means the more stressed you are about money, the worse your financial decisions become. Small automated actions break this cycle. Setting up an automatic weekly transfer of even $25 to a business emergency fund does two things: it builds a real financial cushion, and it trains your nervous system to associate financial action with safety rather than threat.

Habits that support lasting financial health include:

- Scheduled money dates: Weekly 30-minute reviews of cash, revenue, and costs, done without judgment.

- Automated savings transfers: Small, consistent amounts moved to a separate account every week.

- Pricing audits: Reviewing your rates every quarter against your actual costs and market value.

- Boundary-setting with clients: Enforcing payment terms consistently, which reflects your money identity in action.

- Energy clearing practices: Working with abundance rituals for business owners to release energetic patterns that keep financial stagnation in place.

Pro Tip: After completing any financial task you previously avoided, write one sentence: “I did this because I am someone who manages money well.” This identity reinforcement is more powerful than affirmations alone. It anchors the new belief to a real action you just took.

The practical result of this integration shows up in pricing, collections, and investment decisions. Owners who have done the identity work charge what their work is worth. They follow up on overdue invoices without guilt. They invest in growth without panic. These are not personality traits. They are the natural output of aligned beliefs and consistent financial behavior.

Key Takeaways

Removing financial blockages in business requires addressing both subconscious money beliefs and broken operational systems at the same time, with structured action producing measurable results within 30–90 days.

| Point | Details |

|---|---|

| Mindset drives behavior | Subconscious money stories cause avoidance of invoicing, pricing, and financial reviews. |

| Visibility is the first fix | Subdividing bank accounts and completing a 48-hour cash assessment reveals the true problem. |

| Collections beat cost-cutting | Accelerating receivables delivers faster cash relief than reducing expenses alone. |

| Structured triage works | A 30-day triage plan stabilizes cash; 90 days builds systems that prevent the next crisis. |

| Identity change sticks | Combining nervous system regulation with aligned financial actions creates lasting results. |

What I have learned from working with financial and energetic blockages

Most business owners I have worked with arrive believing their problem is purely financial. They want a spreadsheet fix. What they discover is that the spreadsheet was never the problem. The problem was the belief that made them avoid the spreadsheet for six months.

The most overlooked mental barrier is not fear of failure. It is fear of success. Owners unconsciously self-sabotage when revenue starts to climb because abundance feels unfamiliar or unsafe. This is not a metaphor. It shows up as missed follow-ups, underpriced proposals, and sudden “emergencies” that drain cash right when things start to improve.

The practical fix is not willpower. It is structure. When you build systems that run whether you feel confident or not, such as automated invoicing, weekly reviews, and subdivided accounts, you remove the moment-to-moment decision that your nervous system can sabotage. The system carries you through the resistance.

What I have found works best is a dual commitment: do the inner work and do the outer work in the same week. Journal about your money story on Monday. Send the overdue invoice on Tuesday. Review your cash position on Friday. The combination builds evidence that you are someone who handles money well. That evidence rewires the belief faster than any affirmation.

Small business owners who treat financial recovery as both an operational and an energetic project get results that last. Those who treat it as only one or the other tend to cycle back to the same blockages within a year.

— Psychic

Motherodessa’s approach to financial abundance and clearing

Financial blockages carry both a practical and an energetic dimension. Motherodessa has spent over 40 years working with clients across the world to address the energetic roots of financial stagnation, using personalized rituals grounded in West African healing traditions.

For business owners ready to address both layers, Motherodessa offers a Money and Abundance Ritual designed to clear the energetic patterns that keep financial growth blocked. Her Debt Clearing and Release Ritual works specifically on releasing the energetic weight of financial obligation. Every ritual is personalized to your situation. No two sessions are the same. If you are ready to work on the energetic side of your financial recovery, Motherodessa’s money and abundance services offer a direct path forward.

FAQ

What does it mean to remove financial blockages in a business?

Removing financial blockages means identifying and clearing both operational cash flow problems and subconscious money beliefs that prevent consistent revenue and growth. The process combines practical financial management with mindset work for lasting results.

How quickly can a business see results from a financial turnaround?

Businesses can see measurable financial improvements within 30 days by focusing on cash preservation and receivables acceleration. Sustainable systems are typically in place within 90 days.

What is the fastest way to improve business cash flow?

The fastest improvement comes from accelerating collections on outstanding invoices, particularly those over 15 days old. Switching to electronic invoicing can reduce payment collection times by up to 80%.

How do money blocks affect small business owners specifically?

Money blocks cause owners to avoid invoicing, underprice their services, and delay financial reviews, all of which directly reduce cash flow. These behaviors are driven by subconscious beliefs, not a lack of financial knowledge.

Can spiritual practices support financial recovery in a business?

Spiritual practices that address energetic patterns, such as abundance rituals and energy clearing, complement practical financial strategies by targeting the belief-level causes of financial stagnation. Motherodessa specializes in personalized rituals designed for exactly this purpose.