Financial curses pass through family lines because families unconsciously inherit emotional money systems, fixed roles, and unspoken beliefs that repeat across generations. This is not mysticism. It is psychology. Researchers like Dr. Ronit Lami and financial therapist Annie Wright have documented how inherited emotional money roles shape financial behavior below conscious awareness. The formal term for this is intergenerational financial transmission, and understanding it is the first step toward changing it. The patterns feel like a curse because they are invisible, automatic, and nearly impossible to break without knowing what you are actually fighting.

Why financial curses pass through family lines

Every family runs on an emotional system. That system assigns roles, and those roles govern how money flows. Dr. Ronit Lami’s research identifies three core roles that repeat across generations: the provider, the dependent, and the stabilizer. The provider earns and controls. The dependent receives and defers. The stabilizer manages conflict and keeps the peace financially. These roles feel natural because they were modeled from birth.

The critical insight is that these roles are not about money. They are about emotions like control, responsibility, and fear. Money becomes the vehicle for expressing those emotions. A parent who grew up poor may become a compulsive provider, not because they love giving, but because scarcity once felt like abandonment. Their child learns to receive without building, because that is the role the system assigned.

Wealth can actually mask this dysfunction, making it harder to break. When there is enough money to absorb bad decisions, families never face the pressure that forces change. The dysfunction continues, funded and invisible. This is why some of the most financially troubled families are also among the wealthiest.

Families with financial distress unconsciously recreate emotional money dynamics across generations without recognizing the pattern. The repetition feels like fate. It is actually habit.

Pro Tip: Write down the financial role you played in your family growing up. Were you the one who worried about money, the one who spent freely, or the one who never talked about it? That role is likely still running your financial life today.

What are money scripts and where do they come from?

Money scripts are the unconscious beliefs about money formed in childhood through observation, emotion, and experience. Annie Wright, a licensed psychotherapist specializing in financial anxiety, defines them as the core narratives children absorb before they have the language to question them. They are not taught directly. They are caught.

Here are four of the most common money scripts that repeat across generations:

- Scarcity script: “There is never enough.” Children raised in financially unstable homes internalize this as permanent truth. As adults, they hoard, underspend, or live in chronic financial anxiety even when their income is stable.

- Secrecy script: “We don’t talk about money.” Families that treat finances as private or shameful produce adults who avoid financial planning, ignore debt, and never ask for help.

- Shame script: “Money reveals your worth.” When a family ties financial status to personal value, children grow up either chasing money compulsively or self-sabotaging to avoid the judgment that comes with success.

- Vigilance script: “You must always be watching.” This produces adults who are exhausting to live with financially, checking accounts obsessively and treating every purchase as a potential threat.

Unspoken money scripts formed in childhood operate below conscious awareness and drive inconsistent financial choices in adulthood. That inconsistency is what looks like a curse from the outside. The person earns well but cannot save. They inherit money and lose it within years. The behavior seems irrational because the script driving it is invisible.

Non-verbal transmission is equally powerful. Children do not need to hear “money is dangerous” to believe it. They absorb it from a parent’s tense silence when bills arrive, from whispered arguments behind closed doors, from the way a grandparent counted change at the grocery store. Financial secrecy isolates family members and blocks the honest conversations that could interrupt these cycles.

Pro Tip: Ask yourself: “What did I learn about money before age 10 that I never questioned?” The answer to that question is almost certainly running your financial decisions right now.

Why does inherited wealth disappear so fast?

The statistics on generational wealth issues are stark. Between 70% and 80% of American households will inherit nothing, while the top 1% receives an average inheritance of $719,000. That gap does not just reflect income inequality. It reflects a failure to transfer financial knowledge alongside financial assets.

Even families that do pass down wealth often watch it vanish. Theresa Bartelle’s research on why generational wealth fails points to one central cause: children become financial passengers rather than financial drivers. They receive assets without receiving the values, habits, or knowledge that created those assets. The money disappears within one to two generations because the heirs were never taught to drive.

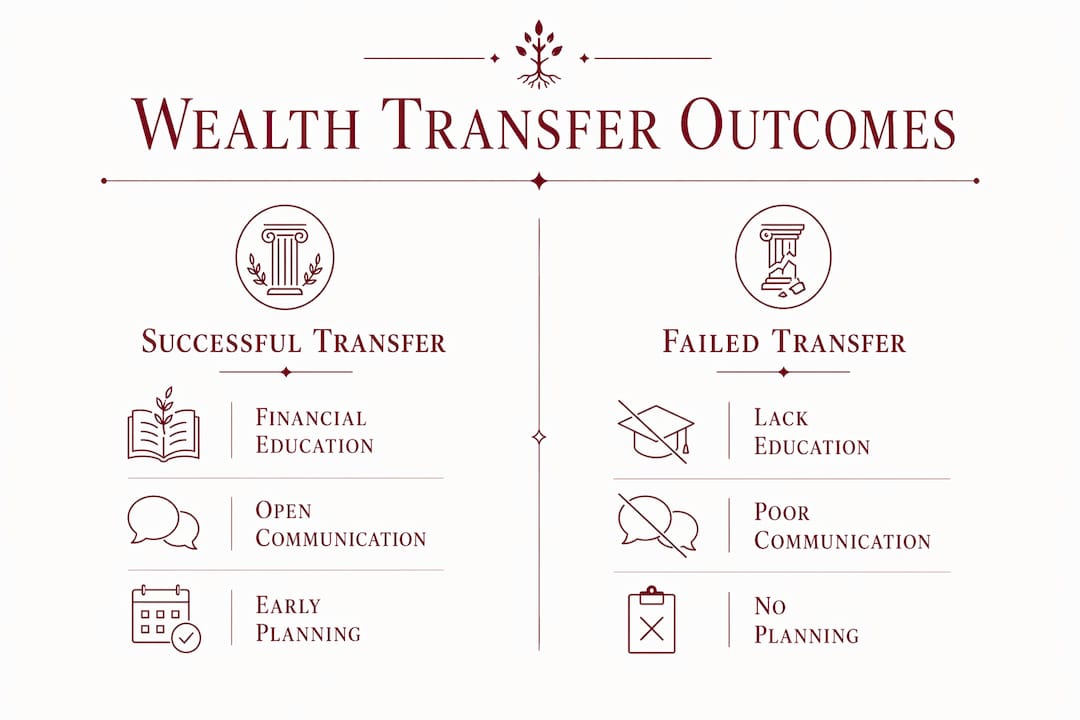

The table below shows the difference between families that successfully transfer wealth and those that do not.

| Factor | Successful Transfer | Failed Transfer |

|---|---|---|

| Financial education | Taught explicitly across generations | Assumed or ignored |

| Communication | Open, regular money conversations | Secretive or avoided |

| Heir preparation | Heirs involved in financial decisions early | Heirs learn only after inheritance |

| Emotional roles | Examined and updated over time | Rigid and unquestioned |

| Values alignment | Shared financial values and goals | Conflicting or unstated values |

The biggest barrier to successful wealth transfer is a lack of communication about money. Families carry enormous emotional weight around finances, including shame, pride, and fear, and that weight produces silence. Silence produces heirs who are financially unprepared. Unprepared heirs produce the next generation of financial dysfunction.

Timing matters too. Research shows that buying a first home by age 30 can increase net worth by 22.5% by age 50 compared to waiting a decade. Families that provide early financial support, whether through down payment help or covering childcare costs, create compounding advantages. Families that withhold that support, often out of their own unexamined money scripts, pass down disadvantage instead.

How do you break a family financial cycle?

Breaking family money cycles requires two things working together: emotional awareness and practical intervention. Neither alone is enough. A person who understands their money scripts but never changes their behavior stays stuck. A person who learns financial tactics without addressing the emotional roles driving their choices will revert under stress.

Here is a practical framework for interrupting inherited financial patterns:

- Name your inherited role. Identify whether you were the provider, dependent, or stabilizer in your family system. Recognize that this role was assigned, not chosen.

- Surface your money scripts. Write out the beliefs about money you absorbed before age 12. Challenge each one with evidence from your actual adult life.

- Start the conversation. Open financial dialogue with family members, even if it feels uncomfortable. Financial secrecy perpetuates dysfunction across generations. Naming the pattern out loud begins to dissolve it.

- Build financial education deliberately. Read books like The Psychology of Money by Morgan Housel or work with a financial therapist who understands intergenerational patterns.

- Consider ritual and ceremony. For many families, especially those rooted in spiritual traditions, a generational curse breaking ceremony provides the emotional and spiritual reset that purely intellectual approaches cannot reach.

Breaking financial patterns requires intentional intervention to interrupt unconscious emotional money roles. Awareness is the entry point. Action is what changes the outcome. You can also explore money manifestation offerings rooted in West African tradition as a complementary path toward shifting your financial energy.

Pro Tip: Schedule one honest money conversation with a family member this month. Not about budgets or bills. About what money meant in your household growing up. That single conversation can surface decades of inherited scripts.

Key takeaways

Generational financial patterns persist because emotional money roles, unspoken scripts, and communication failures pass down more reliably than assets do.

| Point | Details |

|---|---|

| Emotional roles drive patterns | Families assign provider, dependent, and stabilizer roles that repeat across generations unconsciously. |

| Money scripts start in childhood | Beliefs formed before age 12 drive adult financial behavior, often without conscious awareness. |

| Wealth disappears without knowledge | Heirs who receive assets without financial wisdom become financial passengers and deplete wealth fast. |

| Silence is the real curse | Lack of communication about money is the single biggest barrier to successful wealth transfer. |

| Change requires dual action | Breaking cycles demands both emotional awareness of inherited roles and deliberate financial education. |

What 40 years of watching families and money taught me

I have sat with hundreds of people who believed their financial struggles were personal failures. They were not. Every single one of them was running a script written before they were old enough to read. The most heartbreaking cases were the ones who had actually built something, only to watch it unravel because they never examined the emotional system underneath their success.

The pattern I see most often is this: a family breaks out of poverty in one generation through sheer discipline and sacrifice. The next generation grows up with more comfort but absorbs the anxiety that created it. By the third generation, the anxiety is still there but the discipline is not. The money is gone, and nobody understands why.

What I have found is that financial tactics alone will not fix this. You can give someone a budget, a savings plan, and a financial advisor, and they will still self-sabotage if their inherited money script says they do not deserve stability. The emotional work has to come first, or at least alongside the practical work.

The good news is that generational curses are more accurately generational patterns transmitted by behavior and trauma. That means they are changeable. Every pattern that was learned can be unlearned. Every role that was assigned can be reassigned. The families I have seen break these cycles share one quality: they were willing to look honestly at what they inherited and choose something different.

— Psychic

Ready to break your family’s financial pattern?

If this article resonated with you, the work does not stop at awareness. Motherodessa has spent over 40 years helping individuals and families clear the spiritual and emotional weight that keeps financial dysfunction alive across generations. Her approach is personal, private, and rooted in West African healing traditions that address the root causes, not just the symptoms.

Whether you are carrying inherited debt, blocked abundance, or a pattern of financial loss that no budget has been able to fix, Motherodessa’s spiritual healing services offer a path forward. Her Money and Abundance Ritual and Debt Clearing and Release Ritual are designed specifically for people ready to stop repeating what their family handed them.

FAQ

What causes financial curses to repeat across generations?

Financial curses repeat because families unconsciously pass down emotional money roles, unspoken beliefs, and communication patterns that shape financial behavior. These inherited systems operate below conscious awareness and recreate the same outcomes regardless of income level.

Can wealthy families still have financial curses?

Yes. Wealth can mask emotional dysfunction by absorbing the consequences of bad financial decisions, which prevents the natural pressure that forces change. The dysfunction continues across generations, funded but unaddressed.

What is a money script and how does it affect me?

A money script is an unconscious belief about money formed in childhood through observation and emotional experience. Scripts like scarcity, secrecy, or shame drive adult financial choices inconsistently and often self-destructively without the person recognizing the source.

Why does generational wealth disappear by the third generation?

Generational wealth fails because assets are transferred without the knowledge, values, and habits that created them. Heirs become financial passengers rather than drivers, and wealth depletes rapidly without the wisdom to sustain it.

How do you actually break a family financial cycle?

Breaking the cycle requires naming your inherited financial role, surfacing your childhood money scripts, opening honest family conversations about money, and building deliberate financial education. Spiritual and ceremonial approaches can also support the emotional reset that purely practical methods miss.